Lease vs. Loan

Compare the differences between an equipment lease and a loan with our comparison table and make the right equipment acquisition choice for your business.

See full post

By: James Byrne, Business Advisor and Provincial Director of Forestry & Forest Products at MNP

The effects differ depending on whether you purchase or lease, but the take-home message is the same: financing your equipment can have a significant impact on your bottom line.

Deciding whether to purchase or lease a piece of equipment involves a number of factors: available financing options, the lowest overall cost when tax and discount rates are considered, and which option best suits your cash flow and tax situation. If your company has different lenders with different financial covenants, it is important to understand how purchasing and leasing might impact your financial statements so you can ensure that your decision will not put your financial statements offside with one of your lending institutions.

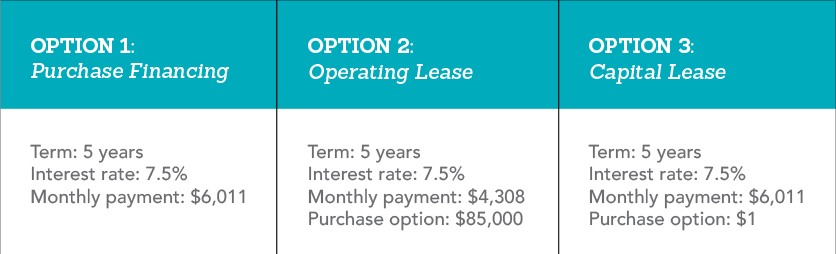

The following example will help you understand what can happen. Let's assume we are considering acquiring a used log loader for $300,000, and that there are three possible means of acquiring the asset. How will the different options affect your company's income statement and tax return?

Accounting: If you purchase the loader, you will control it and it will show as a company asset. Amortization of the loader will occur over its useful life, and the annual amortization (reduction in value) of the asset will be recorded against income. Five years would provide for an amortization rate of 20 per cent. The funds borrowed to purchase the asset will be recorded as a liability. Through the year the principle portion of the loan payments will go against the liability, with only the interest portion being an expense and deducted from operating income.

Tax: Similar to accounting, an asset will be recorded and the associated capital cost allowance (CCA) deducted from taxable income. For accounting purposes, the deduction from income will be based on the estimated useful life of the loader. For tax purposes, CRA will specify the deduction rate based on the type of asset. In this case, the rate would be 30 per cent. As with accounting treatment, loan repayments are not deductible. However, the interest paid will be deducted from taxable income for the period.

Accounting: Financing equipment through leasing typically results in the leasing company recouping their cost of equipment plus a level of profit. The result is a reasonably high financial commitment on a monthly basis for the use of the asset. The asset leased will not be considered yours to control and will neither show up as an asset on your balance sheet nor will a liability be recorded. As you do not record ownership of the loader, your financial statements will not show any amortization expense or interest portion of your payments to the lease company. However, what you will show is the full amount of the lease payments, which will be deducted from the calculation of income.

Tax: For tax purposes there will be no asset controlled, and no CCA deducted. Unlike the purchase option, where only interest is deducted from income, the full amount of the lease payment will be deducted for tax purposes.

Accounting: For capital leases you will be considered to have assumed the benefits and liabilities of ownership of the loader for the term of the lease. This assessment is based on the length of the lease, the total lease payments required, and the ending purchase price. As a result, the loader leased, as well as the liability that must be repaid over the term of the lease, will be recorded on your balance sheet. As control of the loader is assumed, amortization of the loader will be recorded for a capital lease, similar to a purchase. Unlike an operating lease, capital lease payments are treated similar to loan repayments, with only the interest portion of the lease being expensed.

Tax: While the loader will show on your balance sheet for accounting purpose, CCA will not be calculated for tax purposes. However, similar to the operating lease, the full portion of the lease payment is deductible for tax purposes (interest and principal).

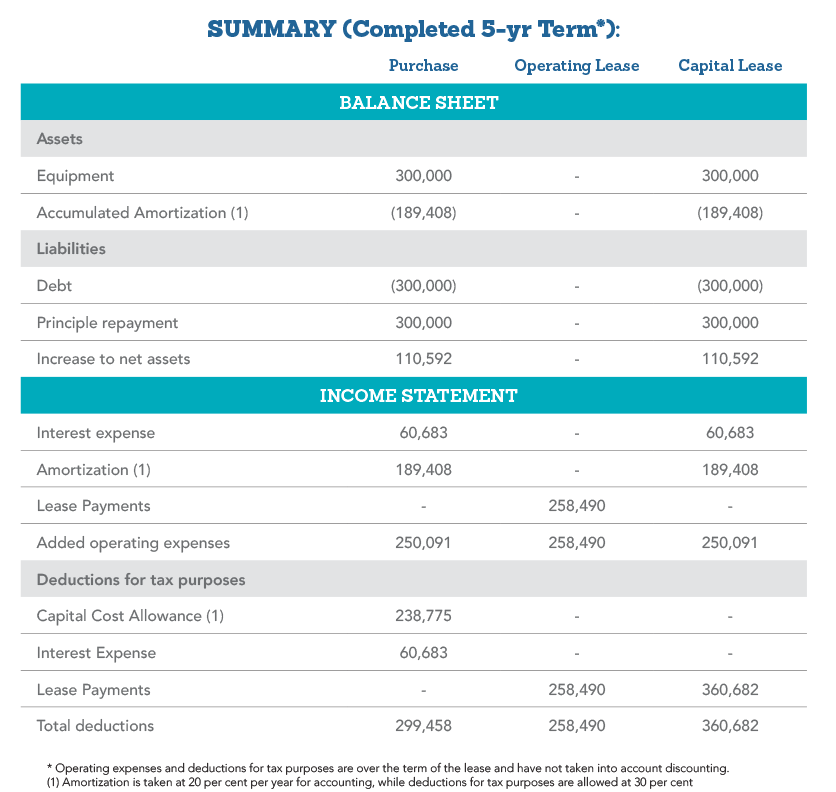

To better illustrate these differences described in the example above the following table summarizes the impact of the various options over their full term.

Lease commitments: Deciding whether to lease or finance new equipment purchases should be done in cooperation with your banking institution. Depending on potential financing covenants (restrictions), the addition of lease obligations can have significant implications to any pre-existing financing requirements. While an operating lease will not show on your balance sheet as a liability, there is still a "commitment" to make payments over the lease term. This commitment to payments is an important factor to most lenders and should be discussed before making any decisions.

Interest rates: Interest rates are a function of risk assumed by the lender. The more security a lender takes reduces their risk and, as a result, should reduce the reward and interest rate charged. If less security is required, the risk to the lender increases and so too does the required return and interest rate charged.

Timing of acquisition: The purchase of a piece of equipment allows for the full amount of CCA to be deducted from taxable income in the year of purchase, regardless of the timing during the year. For operating and capital leases, only the lease payments paid during the year are deductible for tax purposes. This fact will impact the decision on whether the lease or purchase option provides the lowest overall cost. The example above assumes that the acquisition and leases were made at the start of the year.

Your decision on whether to finance or lease your next equipment acquisition is important. It involves numerous factors that will affect not only your current bottom line and tax position, but also has the potential to influence your company's ability to obtain financing in future years. To ensure that you're not limiting your company's opportunities one should ensure that they consult their primary lending institution. Ensuring you make an informed decision is crucial to your success.

James Byrne, BASc, MBA, CPA, CA is a Business Advisor and the Provincial Director of Forestry & Forest Products at MNP | Accounting > Consulting > Tax. Working from MNP’s Nanaimo office, James delivers a broad range of accounting and compliance tax solutions as well as ongoing business and succession planning advice to logging contractors and other businesses linked to the forestry sector. For more information, contact James at 250-734-4320 or [email protected], or view his LinkedIn profile.

MNP is one of the largest accounting, tax and business consulting firms in Canada, offices in more than 80 urban and rural centres across the country. Working with local team members, you have access to our national network of professionals as well as strategic local insight to help you meet the challenges you face every day and achieve your goals. To find an MNP business advisor near you, visit MNP.ca.

This post originally appeared on MNP. This article reflects the views of MNP. For accounting advice specific to your business, speak with your accountant.

Posted in Equipment leasing advice,

Contact us and we'll call you right away